Answering your buyer questions

Some common questions during the real estate process

My business hours are

Monday - Saturday: 9:00 am - 6:30 pm

If you called during business hours and your call was unanswered, it is because I'm probably showing another home, in a meeting, at a closing, working with one of my other agents, I'm outside of my business hours, or spending time with family. I promise that I will get back to you as soon as there is a break in the schedule to give you the full attention and care that you deserve.

Absolutely! I understand that thoughts, ideas, and questions may come up after hours. You're always welcome to text/email after hours. I'll reply during business hours the following day.

To ensure we make the most of our house hunting time together, seeing pre-approved buyers is my standard practice. Here's why it benefits you:

Let's get you pre-approved! It's a quick and easy process that puts you in a strong position to find your dream home.

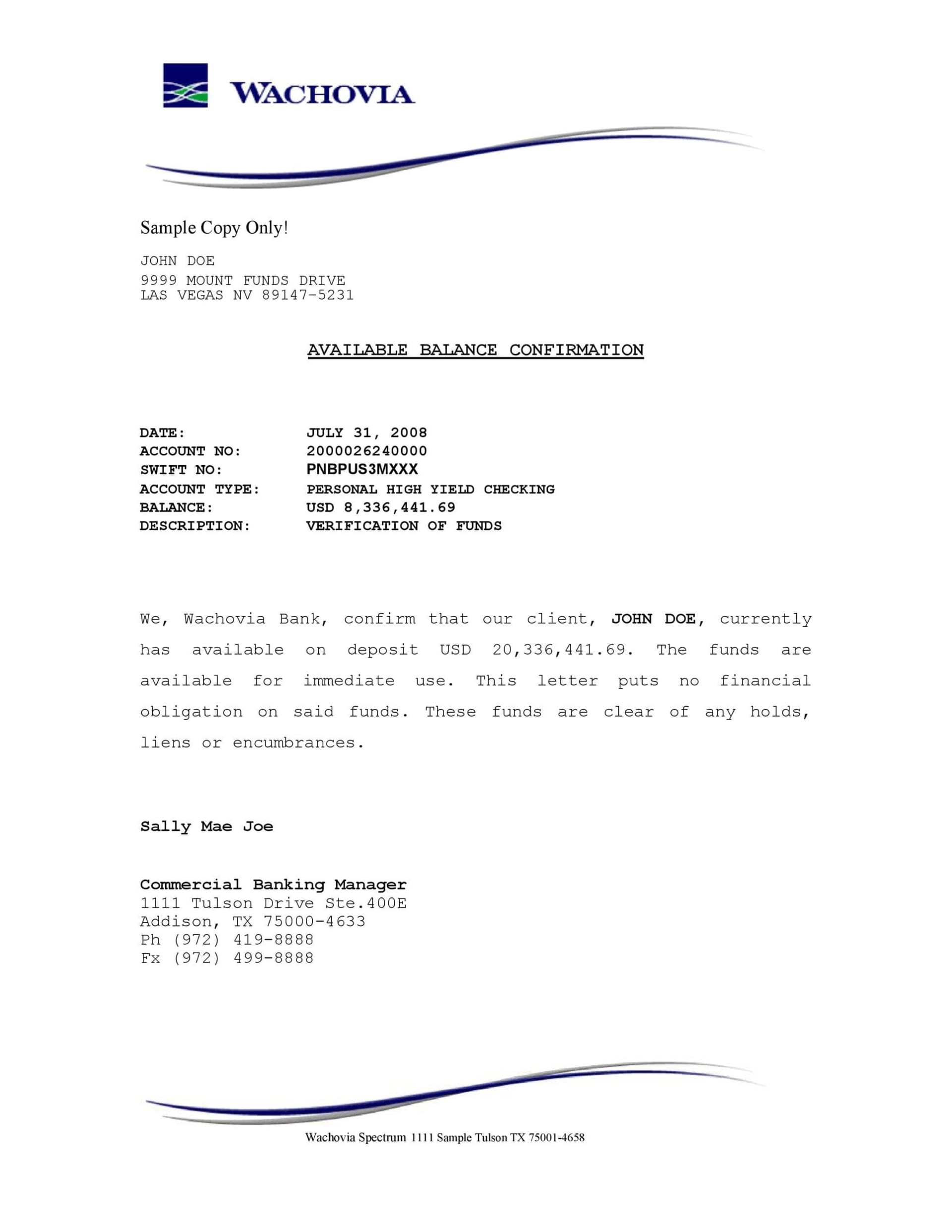

POF example letter from a bank:

I absolutely can! I work with excellent lenders, and they all provide exceptional service!

1) Tyler Carlston, VettedVA - UMortgage - [email protected] - (512) 595-3839

2) Heather Hegle - American Pacific Mortgage - [email protected] - (210) 816-2345

3) LeShawn Nash - Evolution Mortgage - (913) 633-3698

1. Competitive Rates:

The interest rate on your mortgage is a paramount factor that will affect your monthly payments and the overall cost of your home over time.

Different lenders offer varying interest rates. Even a small difference in the rate can translate to substantial savings over the life of the loan

2) Closing Expediency:

The speed at which a lender can close is crucial, especially in a competitive market where sellers favor quick closures.

Inquiring about the average closing times of different lenders can provide a clearer picture and better position you in your home buying journey.

3) Customer Service:

Exceptional customer service throughout the process can make your home buying experience smooth and less stressful.

Look for lenders who are prompt in responding, transparent, and willing to answer your questions.

4. Credit Score Concerns:

A common apprehension among buyers is the potential negative impact on their credit score when shopping around for lenders.

However, credit bureaus recognize the importance of rate shopping and consolidate multiple inquiries into a single 'hit' if done within a 14-day period, thus minimizing the impact on your credit score.

5) Loan Options and Terms:

Lenders offer a variety of loan products with different terms and conditions.

Assessing the loan types, down payment requirements, and other terms from multiple lenders allows you to find a match that aligns with your financial situation and long-term goals.

6. Transparency and Hidden Fees:

Some lenders may have hidden fees or terms that are not favorable to you.

Comprehensive reviews and comparisons among lenders will unveil the full picture, ensuring there are no unpleasant surprises down the line.

7. Local Market Knowledge:

Lenders with a robust understanding of the local market can provide invaluable insights and potentially better service.

Their familiarity with local regulations and market conditions can be a significant advantage.

8) Purchase estimate sheets

This part is crucial with your lender. Before we submit an offer I always want to ensure you know your estimated monthly payment as well as closing costs associated with the home you're interested in. Your selected lender should be able to write one up for you within 30 minutes.

To get pre-approved for a mortgage, lenders typically require various documents to verify your income, assets, and creditworthiness. Here's a breakdown of the common documents you'll need to provide:

Personal Identification:

Proof of Income and Employment:

Financial Assets:

Housing Debt (if applicable):

Additional Documents:

Here are some additional tips:

Homes will be sent in a myriad of ways. The most notable and frequent is from the MLS. The emails will come from a "ConnectMLS" email account. Another great source is directly from our site, BIGRETX.com. We will also ask that you designate us as your agents on Zillow so we can set you up on a search there as well.

If a home is labeled as "assumable," it means you may be able to take over the seller's current mortgage, including their low interest rate. This could save you money if their rate is much lower than current rates. Here are the basics:

Loan Servicer Approval: The seller's loan servicer has to approve you to take over the loan. They’ll check your credit, income, and financial situation.

Eligibility: Assumable loans are often FHA, VA, or USDA loans. Conventional loans are rarely assumable, so we’d check the loan type first.

Down Payment/Bridging the Gap: You’ll likely need to cover the difference between the loan balance and the home’s current price, either with cash or another loan. For example, if the property is listed for $300k and the sellers owe $250k, you'll need to bring $50k to the closing table.

Closing Costs: There are still fees involved, but I'll negotiate to have seller contributions.

VA Approval: Once the seller's loan servicer approves, then the VA must approve you assuming the mortgage.

If this sounds like a good fit, I can help review the details and guide you through the process smoothly!

If allowed by the seller and our schedule has room for it, I will always strive to accommodate tours of homes you're interested in. Properties listed as 'Go & Show' typically have easier access for viewings.

However, homes requiring an appointment may not always be available for same-day tours.

To ensure the smoothest experience, please provide a list of properties you wish to see by the day prior. Any properties added after this list is submitted will be scheduled for a subsequent viewing day.

Absolutely, if we're still within our scheduled showing window, which typically lasts for 30 minutes, we should be fine. However, if you find yourself running more than 15 minutes late, it might be difficult to view the property at this time. Usually, we will have a packed schedule and must honor the time slots allocated for other showings, as the sellers have made specific arrangements. I appreciate your understanding, and I’ll do my best to accommodate you or reschedule if necessary.

Usually, sellers prefer a 24 hour notice prior to showing their home. We ask that you check the "heart" button in the MLS portal. Additionally, you can screenshot the home and send it to me in a text message. In the event we can see the home same day because it's vacant, I'll let you know! Every attempt will be made to accommodate same day appointments, but due to scheduling they can not always be guaranteed. Priortization is key. I understand how stressful it can be to see so many amazing homes. Please send them to me in order of "MUST sees" first.

Absolutely! There are two main ways to tour properties, and I can help you with both depending on your situation:

1. In-Person Tours:

This is the traditional method, where you visit the property yourself and get a feel for the space. You can explore the layout, see the size of the rooms firsthand, and notice details like modern updates or the overall ambiance of the home.

2. Virtual Tours:

Virtual tours are a great option if you can't be there in person. The quality can vary, but I take pride in creating detailed and informative virtual tours that go beyond simple visuals. Here's what sets mine apart:

These details can help you get a good sense of the property's layout and functionality, even from a distance.

Let me know which option interests you more, or if you'd like to discuss both!

The current real estate market is at such an incredibly fast pace that it makes being at every showing very difficult. In the event that I cannot make it to a showing, you may be working with a member of my immediate team or one of our many showing assistants. When viewing homes with a team member or showing assistant, I will still be the one to write the contract, negotiate on your behalf, etc.

Yes! Just like in a preowned transaction, the new build representative works on behalf of the builder. There are some instances where the builder can change your home price during your contract and without a realtor, you may not be able to negotiate that price justification difference. We can also negotiate upgrades for you.

We set our representation agreements in increments of six (6) months. If you feel that at any point you are not receiving the best quality service, we will mutually terminate our relationship agreement.

Earnest Money: This is typically a deposit of 1% of the contracted sales price that shows the seller you're serious about buying the home. The good news is this money gets applied towards your closing costs later on.

Inspection Fees: There are two main inspections to consider:

Option Fee: This fee gives you the exclusive right have inspections, receive contractor bids, and also the ability to terminate the contract and get your full earnest money back. The option fee is typically a small amount, $10 per day.

Here's what comes next in the home buying process:

(We'll discuss these additional costs in more detail as we move forward)

My standard fee for representing buyers is a commission of 3% of the final sale price of the home. In most cases, this commission is paid by the seller, not you.

However, it's important to be aware of recent legal cases regarding real estate commissions. These cases have opened the door for sellers to negotiate the commission rate with the listing agent. If this happens, I will be transparent with you about any difference between my standard fee and the amount the seller offers. We can then discuss how you'd like to proceed, including potentially adjusting my fee or negotiating with the seller's agent to reach a fair agreement.

My goal is to ensure you have a smooth and successful home buying experience. I'm committed to clear communication and advocating for your best interests throughout the process, including navigating any commission discussions.

There are two main ways to get closing costs covered:

Seller concessions: Negotiate with the seller to contribute towards your closing costs. This is common, especially in a competitive market. In some instances the seller will ask us to increase our offer price by the amount we are asking for so they can break even - this is common.

Lender credits: Some lenders offer programs with lower interest rates in exchange for a higher upfront fee that can cover some closing costs.

While we aim to close on the date listed in our contract, closing dates can be flexible due to various factors. It's best to consider it a target date as closing can either be moved up or pushed out.

Here's why:

To be safe, I recommend not scheduling movers or utility changes for the exact closing date. We'll keep you updated throughout the process and let you know as soon as a firm closing date is confirmed. In the meantime, let's tentatively schedule those for a day or two after the target closing date.